Part 1: Smoke and Mirrors: Unpacking Canada's Cobalt 27, Nickel 28 & Blockmint Technologies

When what you read isn’t always what you get in the capital markets

Introduction

Parallel universes

In the high-stakes arena of modern finance—where digital assets and exotic finance structures dangle life-changing returns—three Vancouver companies became textbook cases in perception management. Cobalt 27, Nickel 28, and Blockmint didn’t just operate as public companies; they curated parallel realities: one for the capital markets and retail investors, another for insiders, and financial-system gatekeepers (bankers, attorneys and underwriters).

Over several parts of this story, I will explain the gap between disclosure and reality, and how that gap may have enriched the few at the expense of the many.

At first glance, the first company - Cobalt 27 - appeared revolutionary: it was a pure-play commodities retailer which bought and resold the metal without ever touching a mine or refinery. The second company, Nickel 28, later recycled the same model for nickel, while the third, Blockmint, held itself out to investors as an alleged Blockchain company.

In 2019, Cobalt 27 completed an act of corporate mitosis, and split itself: one half kept the tangible assets (inventory and cash), while the other—Nickel 28—inherited royalties and mine stakes. The shell changed, but the DNA didn’t: same offices, same executives, same structure. Only the commodity narrative shifted.

This series begins with Cobalt 27, moves to Nickel 28, and ends with Blockmint Technologies.

Cobalt 27 Capital Corp.

A Cobalt Empire

In the spring of 2017, Cobalt 27 Capital Corp., a little-known company began circulating through mining investment circles, pitched as “a cobalt ETF on steroids”.1

One of its founders was Michael Beck, an American active in the Canadian capital markets operating under Regent Advisors LLC and Angstrom Capital Ltd., the latter housed offshore at Lines Overseas Management (LOM) in the Bahamas. A decade earlier, LOM had been named in an SEC enforcement action alleging the use of offshore nominee accounts to conceal beneficial ownership in connection with a pump and dump scheme involving Sedona Software Solutions Inc, a Vancouver company.2 The SEC claimed that share purchase agreements and trading records had been backdated. The case settled in 2010.

Cobalt 27 Capital Corp.’s proposition was pure financial alchemy: investors could bet on the battery revolution without dirtying their hands with mines. The cobalt, they claimed, was warehoused and poised to soar in value.3,4 In fact, it was so hot, you could buy Cobalt 27 stock in the US, stick it in your drawer, go to sleep and “wait for the Cobalt 27 Prize.”5

It seemed like the ultimate passive investment for a shareholder, and for the public company - one that required no skilled executives to direct or manage it.

At that time, capital markets promoters were warning that a global shortage of cobalt, a key input in rechargeable lithium-ion batteries, was imminent. The scarcity, some claimed, could derail the electric vehicle boom. Cobalt 27 positioned itself as the solution: a pure play on physical cobalt, with no exposure to mining risk, no geopolitical complications, and no operational surprises.

Investors were told they would capture the upside of rising cobalt prices through the company's stock. More than that, the founders insisted—again and again—that there was only one pure cobalt investment vehicle in the world. Just one. Cobalt 27.6

If you got in, you’d get the “Cobalt 27 Prize.”

As we shall see, the prize proved elusive.

Within just two years, the company would raise hundreds of millions of dollars, barter more than 2,000 metric tons of cobalt from obscure counterparties, and—as suddenly as it appeared—retreat and vanish back into the hands of a Russian oligarch, from whence it had emerged.

Shareholders were left with diluted paper in a different entity, no cobalt inventory, no long-term rise of the cobalt wave, and no cogent explanation.

How did a Canadian public company end up back in the hands of a Russian oligarch? Who were his connections in Canada?

To find that answer, we go to the Kuzbass coal mines of Kemerovo Oblast, Siberia.

Along the way, we’ll pass through some of the stranger corners of Canadian capital markets—the kind of coincidences and crossovers that seem to happen only here.

Is it all connected?7

There’s Connected and Then There’s Connected.

Before we get to Russia, it’s worth taking stock of who was already in the room. The names begin to repeat—quietly at first, then unmistakably.

Many were involved in Uramin Inc., a Canadian uranium company sold in 2007 to the French government for more than $2 billion, a deal that later drew scrutiny from French authorities and was described in the local press as une escroquerie.

Among those involved in Uramin were Stephen Dattels, Michael Beck, Stephen Beck, Ian Burns, Angstrom Capital, Regent Mercantile Bancorp Inc., Ian Stalker, and SRK Consulting8 — names that will reappear.

And some of the overlaps between those behind Cobalt 27, Nickel 28, and Blockmint Technologies border on the surreal.

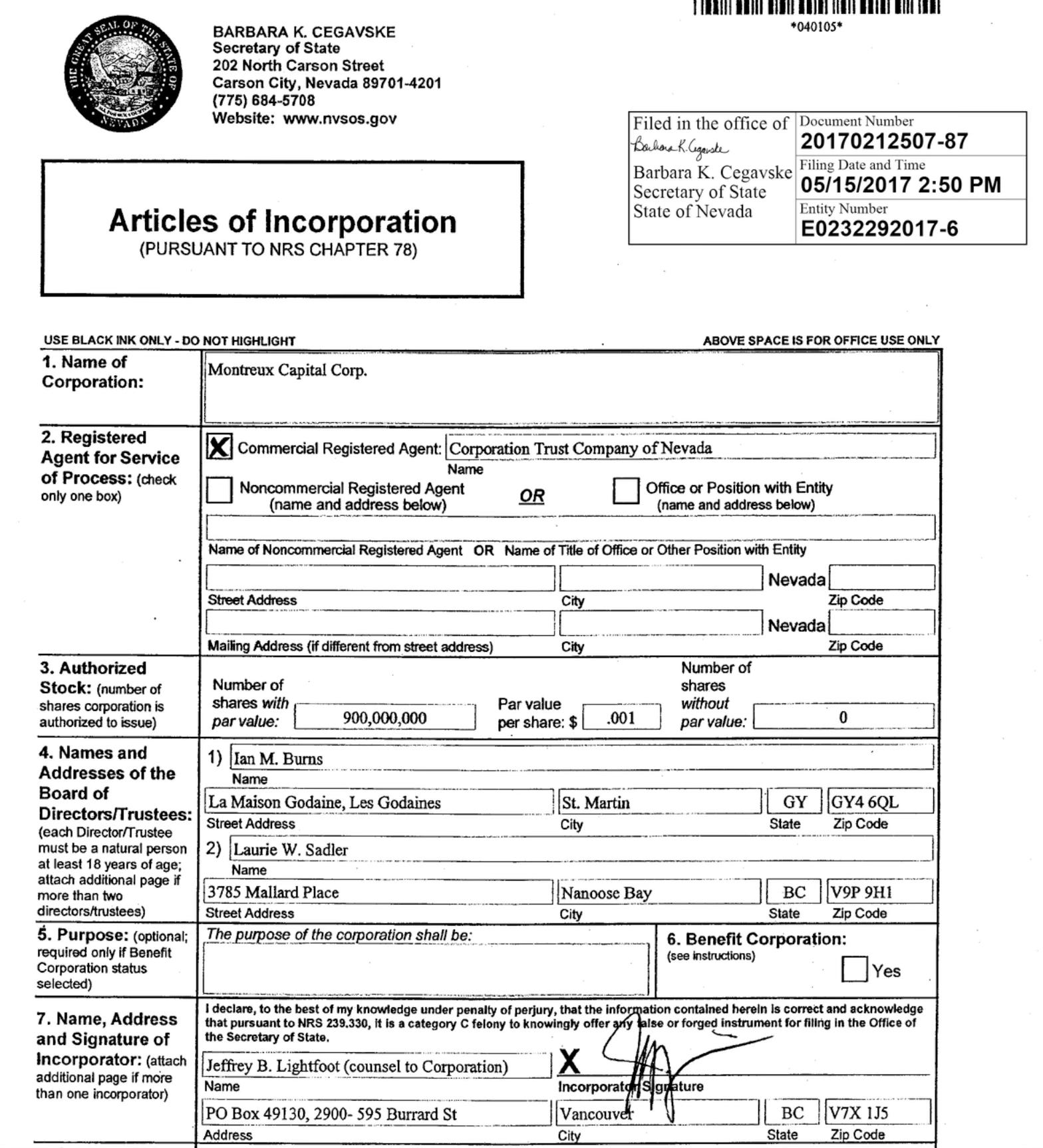

For example: Ian Burns ran a Vancouver issuer called Assure Holdings Corp.,9 formerly Montreaux Capital Corp., which at one time was partially owned by a Vancouver paralegal named Erin Walmesley.10 Its auditor resigned without explanation.

Walmesley later appeared on the management team of another Vancouver issuer alongside Colin Watt,11 and had previously worked for the Vancouver law firm that represented Sedona Software Solutions Inc. —the company at the center of the SEC’s action against LOM. Among the firm’s lawyers was Michael Seifert, then of Maitland & Company.

Watt, Walmesley, LOM, Seifert - these are names we will come across again.

In Part 2, as we explore how the Russian oligarch who co-founded Cobalt 27 made his fortune during the Yeltsin-era privatizations, we learn that his holdings included ownership of a coal mine in the Kuzbass region of Siberia, Russia.

Just 100 miles from that mine in Siberia, another coal deposit—long abandoned and underwater—was sold to investors by a Hong Kong-listed company named Siberian Mining.

SRK Consulting, the firm tied to Uramin, also prepared the assessment for the Siberian mine. Civil complaints filed by Hong Kong investors alleged that this too was une escroquerie.

The man behind Siberian Mining’s pivot from garment manufacturing in China to coal extraction in Russia was Choi Sung-min, a Korean crypto figure. Choi also owned LitheA Inc., which was later acquired by LSC Lithium Corp., a Canadian firm backed by some of the same people behind Cobalt 27. SRK Consulting appeared once more, providing yet another mining report for yet another company with ties to Choi.

In the video clip posted above, Cobalt 27 co-founder Michael Beck is interviewed by Collin Kettell. In May 2019, Kettell received 200,000 shares in BetterLife Pharma Inc., a company where Beck’s group was co-leading a financing. Choi was slated to participate in that same private placement in Vancouver but withdrew at the last minute because, as he told one of the Cobalt 27 insiders, “his mother was sick”.

As our story continues, so does the cast—circling through these companies with the quiet cohesion of a syndicate.

Coming Next: Part 2—Vladimir Iorich, the Russian Oligarch Behind Cobalt 27

“Interview of Michael Beck of Regent Advisory LLC”, YouTube, October 26, 2017.

Securities and Exchange Commission, Complaint, SEC v. Brian N. Lines, et al., No. 05-CV-02485 (SDNY filed March 9, 2005), https://www.sec.gov/litigation/complaints/comp19280.pdf.

“Cobalt 27 faces investor outcry amid accusations its selling crown jewel assets at a loss”, Financial Post, September 6, 2019.

“Investors bought Cobalt 27 for its massive stockpile - now they’re being asked to cash out just as cobalt prices are poised to surge”, Financial Post, October 4, 2019.

“Interview of Michael Beck of Regent Advisory LLC”, YouTube, November 26, 2018.

Ibid.

Video clip from Ms. Mojo YouTube Channel, YouTube.

Iain Adams and Andrew Morrall, Uramin: A Team Enriched – How to Build a Junior Uranium Mining Company (London: Waterstones, 2008); SEDAR filings of UraMin Inc.

Ian Burns, Form 51–102F3 Material Change Report, filed on behalf of Montreux Capital Corp., March 5, 2014, SEDAR, https://www.sedarplus.ca.

Montreux Capital Corp., Final Prospectus, May 27, 2008, SEDAR, https://www.sedarplus.ca.

Colin Watt, Form 51–102F3 Material Change Report, filed on behalf of Conquest Ventures Inc., August 13, 2003, SEDAR, https://www.sedarplus.ca